At Sephora and Ulta, the old price-tier logic is fracturing. A $6 serum sits in the same top-10 as a $99 cream, and the brands that understand why are pulling away from everyone else.

ANALYSIS BASED ON Q1 2026 VS. Q4 2025 DATA:

500+ BRANDS, 5,500+ PRODUCTS TRACKED

BRANDS TRACKED

500+

Ulta & Sephora combined

PRICE TIERS MAPPED

9

Masstige to Luxury

CATEGORIES ANALYSED

12+

Serums to Suncare

The conventional wisdom in prestige beauty has always been that price tier and rank tier move together. Spend more, rank higher. Carry a heritage brand name and the shelf takes care of itself.

Q1 2026 data from Sephora and Ulta tells a more complicated, and a more interesting story.

At Sephora, the overall skincare brand ranking is led by rhode, Hailey Bieber’s affordable brand priced largely between $20–$30, which holds the #1 overall position with 9 products in the top 50 and 10 in the top 100. Right behind it, at #2, sits The Ordinary, a masstige label whose bestsellers range from $6 to $17. Both are outranking Drunk Elephant & Tatcha.

Bestsellers usually follow a demand curve between price and volume. A lower price tier is likely to rank above a higher-tier brand or SKU because of the volume that a brand can tap. But, this only tells part of the story. Rhode is an affordably priced brand with median price of $20-$30 and yet ranks above all the masstige brands like The Ordinary, Beauty of Joseon and Tower 28.

Why?

Of course, Rhode has a much healthier reach because of Hailey’s celebrity status, but higher ranks also come down to number of hero products and percentage retention.

Rhode has a much higher percentage of Top 50 products versus the masstige brands even though the total products don’t vary by much versus them. Also, even though Rhode has not launched any disruptive innovation, the massive top of the funnel appeal as well as the quality of formulations are likely resulting in much higher retention for the brand.

Lastly, Hailey Bieber has brought in new & younger consumers to Sephora, which they must have counted on, the social and store investments would likely be much higher and thus resulting in much higher support from the retailer.

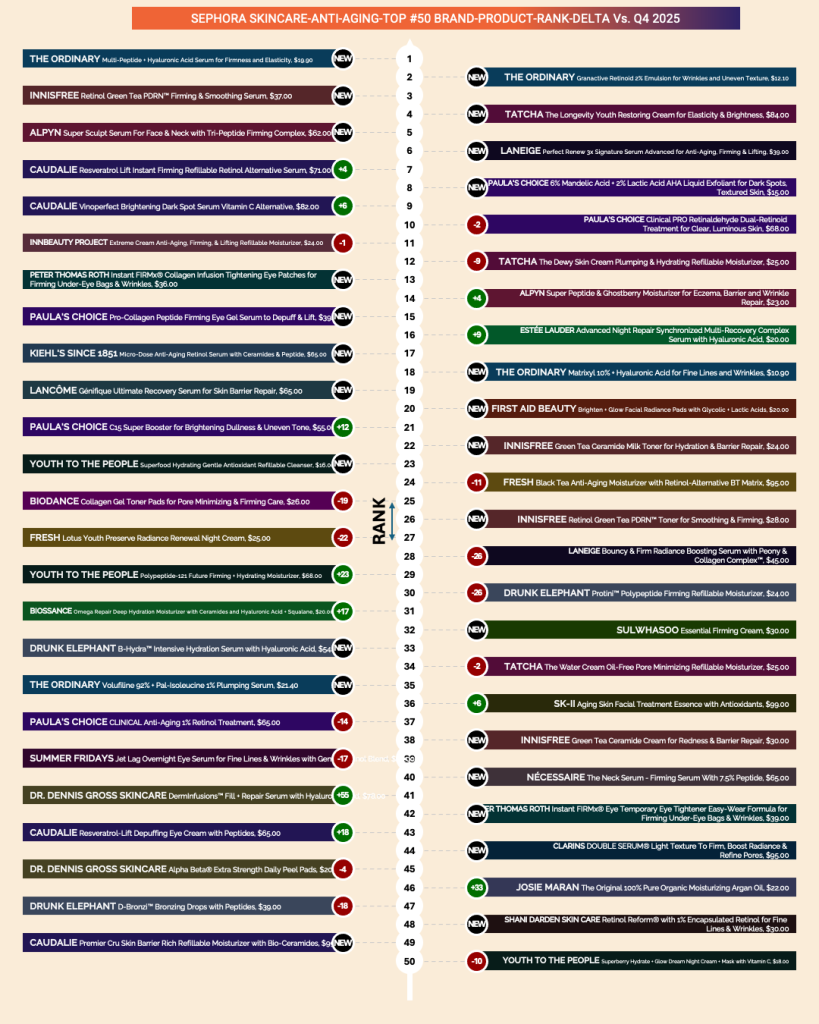

The Anti-Aging Category: Where Prestige still has Power, and Where it's slipping

Anti-aging remains the one category where prestige and luxury pricing still command top placement. The Sephora anti-aging top 20 reads like a who’s who of clinically-positioned brands: Innisfree, Tatcha, Alpyn, Paula’s Choice, Caudalie, Estée Lauder.. But within that category, the momentum data reveals a fault line.

| Brand | Product | Price | Rank | Change | Signal |

|---|---|---|---|---|---|

| The Ordinary | Multi-Peptide + HA Serum | $19.90 | #1 | NEW | Debut at #1 |

| The Ordinary | Granactive Retinoid 2% Emulsion | $12.10 | #2 | NEW | Second SKU in top 2 |

| innisfree | Retinol Green Tea PDRN Serum | $37.00 | #3 | NEW | Affordable clinical entrant |

| Tatcha | Longevity Youth Restoring Cream | $84.00 | #4 | NEW | Luxury debut |

| ALPYN | Super Sculpt Serum | $62.00 | #5 | NEW | Prestige newcomer |

| Laneige | Perfect Renew 3x Signature Serum | $39.00 | #6 | NEW | Premium new entry |

| Caudalie | Resveratrol Lift Retinol Alt. Serum | $71.00 | #7 | +4 | Powerhouse leader |

| Caudalie | Vinoperfect Dark Spot Serum | $82.00 | #9 | +6 | Powerhouse leader |

| Paula’s Choice | Clinical PRO Retinaldehyde Treatment | $68.00 | #10 | −2 | At-risk leader |

| Estée Lauder | Advanced Night Repair Serum | $20.00 | #16 | +9 | Emerging disruptor |

| fresh | Black Tea Anti-Aging Moisturizer | $95.00 | #24 | −11 | At-risk challenger |

| fresh | Lotus Youth Preserve Night Cream | $25.00 | #27 | −22 | At-risk challenger |

| Youth To The People | Polypeptide-121 Moisturizer | $68.00 | #29 | +23 | Emerging disruptor |

| Drunk Elephant | Protini Polypeptide Moisturizer | $24.00 | #30 | −26 | At-risk challenger |

| Dr. Dennis Gross | DermInfusions Fill + Repair Serum | $78.00 | #41 | +55 | Highest momentum SKU |

What stands out is not just who’s rising, but how they’re rising. Innisfree’s gains in anti-aging come from a Retinol + Green Tea PDRN Serum priced at $37, a product that speaks the same clinical language as a $68 Paula’s Choice serum, but without the prestige tax. Caudalie too is advancing on the strength of its “retinol alternative” positioning, a deliberate pivot that lets it compete on ingredient story rather than heritage alone.

The price of entry to the anti-aging top 20 is not a luxury price point – it’s a credible ingredient story.

Drunk Elephant’s −26 slide and fresh’s continued decline are instructive. Both carry strong brand equity and genuine product quality. But in a market where The Ordinary debuted a Multi-Peptide + Hyaluronic Acid Serum at $19.90 straight into the #1 anti-aging rank this quarter, with a second SKU landing at #2 simultaneously, premium positioning without a clear clinical differentiation is not enough to hold rank.

Luxury and prestige SKUs like Caudalie’s Vinoperfect Brightening Dark Spot Serum Vitamin C Alternative (Rank 7, +4), Dr. Dennis Gross’s DermInfusions Fill + Repair Serum (Rank 40, +55) with Hyaluronic Acid, and Youth To The People’s Polypeptide-121 Future Firming + Hydrating Moisturizer (Rank 29, +23) not only hold top-50 positions but carry the highest momentum in the category — a signal of sustainable performance driven by product quality that earns strong consumer retention and active retailer support.

The Overall Ranking: Affordable is Not the Same as Low Quality.

The broader Sephora ranking adds another layer of nuance. rhode, ranked #1 overall, is classified as “Affordable” in price tier but its branding & architecture is anything but massy. It commands a lifestyle premium through Hailey Bieber’s cultural positioning, a tightly edited SKU count (17 total products), and a coherent “glazed skin” ritual that gives each product a role to play. The overall value to the consumer is affordable-premium+ at an affordable price, a distinct construct from drugstore affordable.

The Ordinary, in seeming contrast, operates in true masstige: 60 total products on Sephora, $6–$17 price points, ingredient transparency as the entire brand promise. Its top-10 is anchored by the Niacinamide 10% + Zinc Serum and Glycolic Acid Toner, functional heroes with near-zero emotional overlay. Two very different value equations, occupying the same price neighbourhood, both winning at the top of the chart. But, in terms of winning fundamentals, The Ordinary too offers quality comparable or better than some of the affordable brands at masstige price.

Meanwhile, Glow Recipe (Affordable Premium, ranked #5) and Summer Fridays (Affordable Premium, ranked #8) represent a third model: ingredient-led, K-beauty influenced, joyful in visual identity, and disciplined on price. Their top products cluster in the $16 – $29 range. Neither is cheap, but both feel earned rather than premium for its own sake. Both Glow Recipe and Summer Fridays offer premium, perceived quality at an affordable premium price. Fundamentals are forever.

Summary: What This Means for Founders, Retailers, Innovators And Investors

The data, read clearly, suggests three things.

First, ingredient credibility has become the primary currency across all price tiers – from The Ordinary’s blunt actives to Caudalie’s retinol alternatives to Paula’s Choice clinical retinoids. Brands without a clear ingredient-to-benefit story are losing ground regardless of price.

Second, the “masstige squeeze” is real but nuanced: it is not that affordable brands are winning and prestige brands are losing. It’s that affordable brands with strong ingredient stories are winning, and prestige brands without them are losing.

Third, portfolio breadth matters less than portfolio penetration. Having 60 SKUs (The Ordinary) or 12 (Drunk Elephant) is less important than how many of those SKUs break into the top 50 or top 20. Concentration of ranking power, not product count, separates the dominant from the merely present.

For investors, innovators and founders watching category velocity into 2026, the signal from this data is clear:

price tier is increasingly a strategic variable, not a fixed identity. The brands gaining ground are the ones that have chosen their tier deliberately, built an ingredient-backed story commensurate with it, and launched SKUs with enough focus to penetrate top rankings rather than simply populate shelf space.

Source: Jump Accelerator Q1 2026 vs. Q4 2025 Skincare Ranking Report: Ulta & Sephora. 500+ brands, 5,500+ products, 12+ categories, 9 price tiers tracked. Analysis covers Sephora overall, anti-aging, and momentum classifications. Data reflects brand-product rank changes Q4 2025 → Q1 2026.

Beauty reports & solutions for speed of sticky scale| 70+ brands grown