At Sephora, a Premium-Prestige French salon brand holds #1 while a biotech repair brand with 14 products holds #2. At Ulta, a $6.50 shampoo and a $191-rank-climbing scalp microbiome formula are both ascending simultaneously. Two of America’s most important beauty retailers, selling to overlapping but distinct consumers, and their haircare rankings tell fundamentally different stories about where the category is going.

ANALYSIS BASED ON Q1 2026 VS. Q4 2025 DATA:

350+ BRANDS, 7,700+ PRODUCTS TRACKED

BRANDS TRACKED

350+

Ulta & Sephora combined

PRICE TIERS MAPPED

9

Masstige to Luxury

CATEGORIES ANALYSED

14+

Shampoo & Conditioner to Scalp Treatment

The temptation when reading dual-retailer data is to look for confirmation: a single coherent narrative that both channels validate. The Q1 2026 haircare data from Sephora and Ulta resists that temptation. Read together, these two rankings do not simply amplify the same signal. They reveal that the same consumer need – healthy, repaired, beautiful hair – is being served by radically different brand architectures, at different price tiers, through different value propositions, depending on which door she walks through.

Understanding that divergence is where the real strategic intelligence lives.

The Two Leaderboards: A Tale of Two Retail Philosophies

Start with the overall top 10 at each retailer and the structural contrast is immediately apparent.

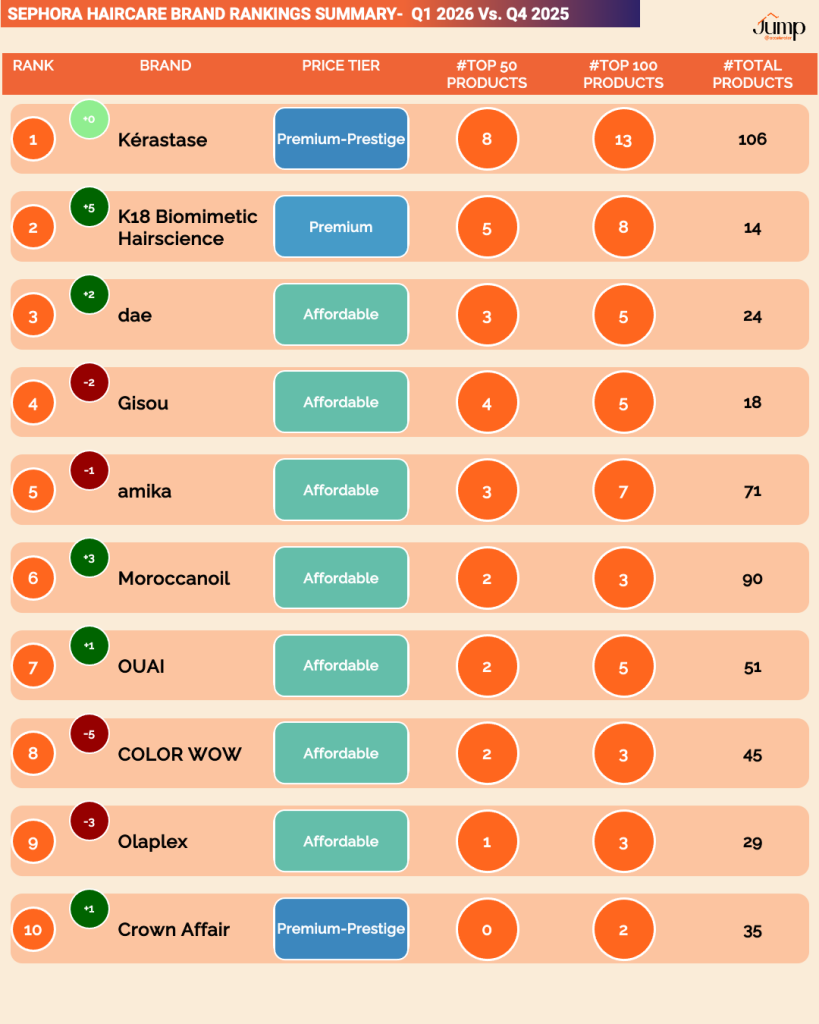

At Sephora,

the top 10 in Q1 2026 is: Kérastase (Premium-Prestige, #1, +0), K18 Biomimetic Hairscience (Premium, #2, +5), dae (Affordable, #3, +2), Gisou (Affordable, #4, -2), amika (Affordable, #5, -1), Moroccanoil (Affordable, #6, +3), OUAI (Affordable, #7, +1), COLOR WOW (Affordable, #8, -5), Olaplex (Affordable, #9, -3), Crown Affair (Premium-Prestige, #10, +1).

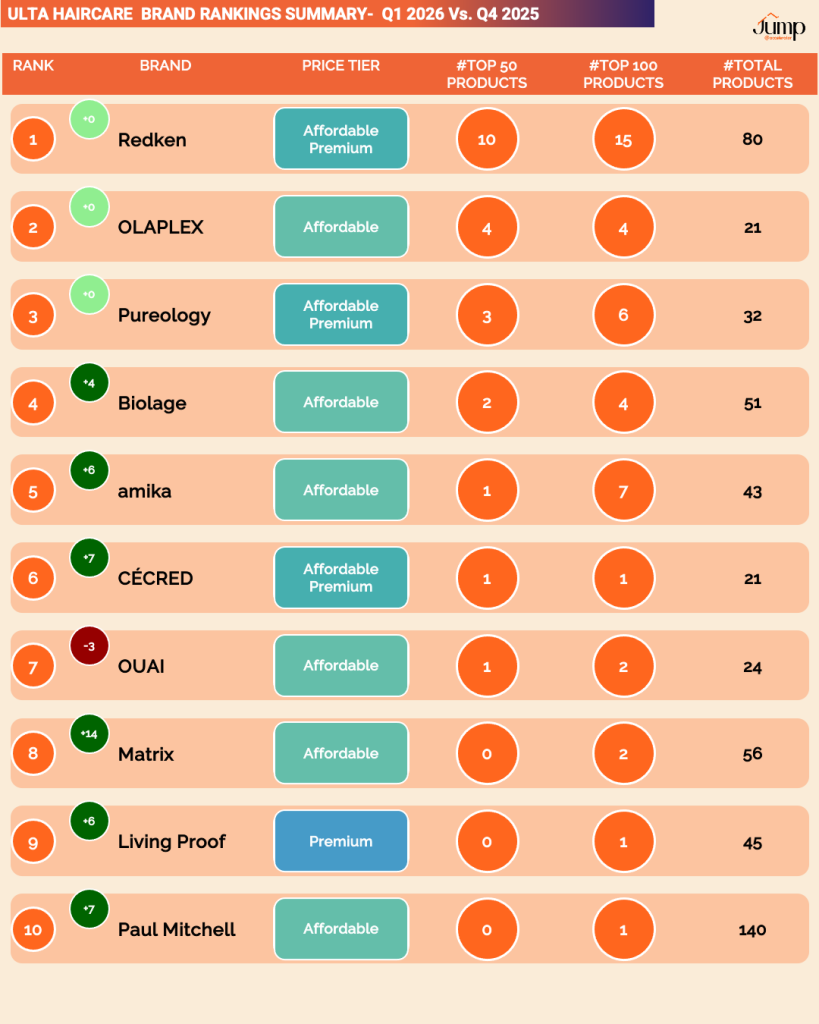

At Ulta,

the top 10 reads entirely differently: Redken (Affordable Premium, #1, +0), Olaplex (Affordable, #2, +0), Pureology (Affordable Premium, #3, +0), Biolage (Affordable, #4, +4), amika (Affordable, #5, +6), CÉCRED (Affordable Premium, #6, +7), OUAI (Affordable, #7, -3), Matrix (Affordable, #8, +14), Living Proof (Premium, #9, +6), Paul Mitchell (Affordable, #10, +7).

The Sephora list includes a Premium-Prestige French atelier, a biotech repair brand, a desert-lifestyle indie, and a honey-provenance storyteller. The Ulta list is built almost entirely on professional salon heritage – Redken, Pureology, Biolage, Matrix, Paul Mitchell – with performance-focused anchors like Olaplex and an emerging disruptor in CÉCRED. Only amika and OUAI appear in both top 10s.

This is not a trivial difference. It maps to a genuine consumer distinction:

–Sephora’s haircare shopper skews discovery-oriented, willing to pay for narrative and novelty alongside performance.

–Ulta’s haircare shopper is more value-anchored, more brand-loyal to salon heritage, and more likely to be buying the same product she has used for years at a price point she can justify on a regular repurchase cadence. The retail channel itself is shaping the brand hierarchy, not just reflecting it.

What Both Retailers Agree On: The Universal Principles

Before examining the divergences, it is worth naming what both datasets confirm, because, the patterns that hold across both channels are the most durable signals in the market.

amika is the only brand in the top 5 at both retailers.

Sitting at #5 at Sephora (−1) and #5 at Ulta (+6), amika has accomplished something rare in beauty retail: genuine cross-channel resonance. Its brand promise – fun, vibrant haircare with professional results for every hair type – is elastically positioned enough to work in Sephora’s discovery environment and Ulta’s loyalty-driven one simultaneously.

Amika’s positioning spectrum spans clean and superfruit ingredients through salon-grade functional benefits, and its product range

(43 SKUs at Ulta Vs. 71 at Sephora)

is calibrated for breadth without losing the brand’s coherent, joyful identity.

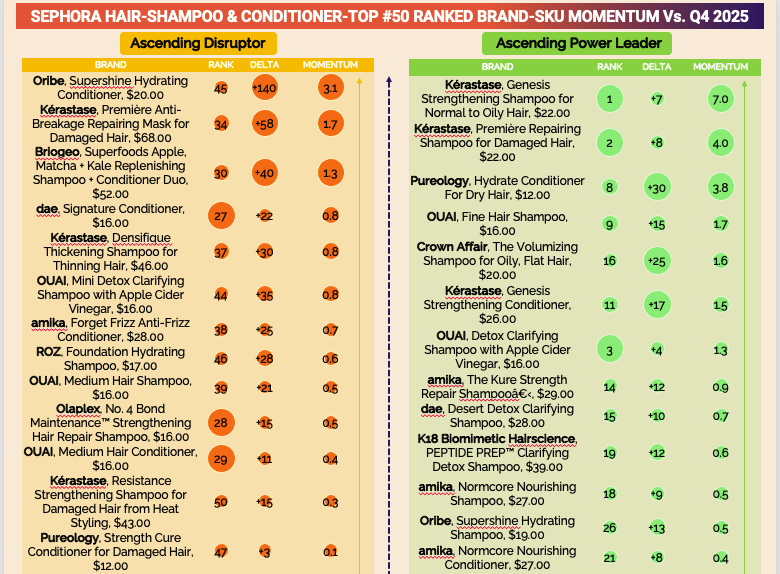

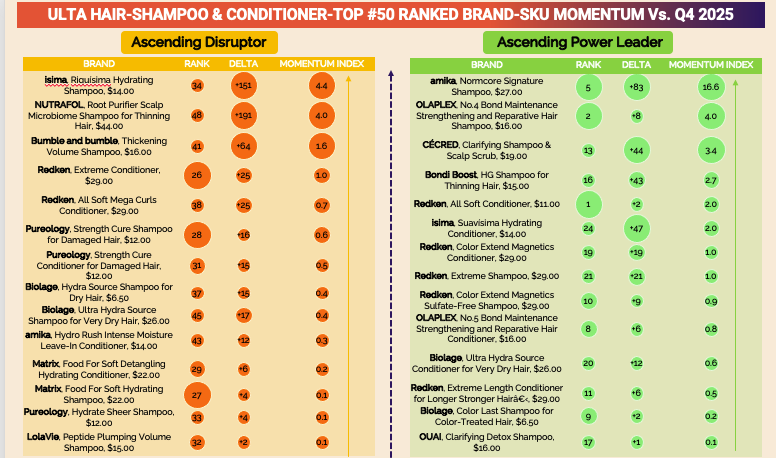

At Ulta, amika’s Normcore Signature Shampoo posted the single most dramatic momentum score in the shampoo and conditioner category: +83 ranks to #5 with a momentum index of 16.6, an Ascending Power Leader by a significant margin.

At Sephora, its Kure Strength Repair Shampoo and Normcore Nourishing Shampoo are both classified Ascending Power Leaders. Same brand, same product range, winning through different mechanisms at each retailer.

OUAI appears in both top 10s .

#7 at Sephora (+1) and #7 at Ulta (-3). Its Affordable pricing and lifestyle-forward positioning give it reach across both channels, though Ulta shows a modest slide that warrants monitoring.

At Sephora specifically, three OUAI shampoos are climbing simultaneously in shampoo and conditioner: the Detox Clarifying Shampoo with Apple Cider Vinegar holds #3 (+4 ranks), Fine Hair Shampoo climbs to #9 (+15), and Medium Hair Shampoo reaches #39 (+21).

The pattern is consistent: benefit-specific naming at accessible price points ($16 across the range) is generating multiple concurrent ascending SKUs within a single brand – a portfolio strategy that is clearly working at both retailers.

Olaplex holds #2 at Ulta and #9 at Sephora – elevated at the value-oriented channel, more challenged at the prestige one.

This divergence is instructive.

At Ulta, Olaplex’s patented bond-repair technology story, delivered at $16 for core shampoo and conditioner SKUs, resonates strongly with a consumer who trusts the brand’s professional heritage and responds to its functional claim. The No.4 Bond Maintenance Shampoo at Ulta has a momentum score of 4.0 as an Ascending Power Leader.

At Sephora, Olaplex is still in the top 10 overall but sliding three places, and its shampoo sits at #5 in the S&C category with a -1 delta. The data suggests Olaplex’s narrative – built on bond chemistry – faces stiffer competition at Sephora from K18’s newer and arguably more specific molecular repair story, while retaining a commanding position at Ulta where that heritage credential still holds decisive authority.

Benefit specificity drives momentum at both retailers, without exception. The Ascending Power Leaders and Ascending Disruptors at each retailer universally share one trait: they name a precise problem and a precise solution.

At Sephora, Kérastase’s Genesis Strengthening Shampoo for Normal to Oily Hair (not simply “strengthening shampoo”) holds the #1 position in shampoo and conditioner with a momentum score of 7.0.

Pureology, hydrate conditioner for dry hair and Crown Affair, the volumizing shampoo for oily, flat hair show the highest rank gains respectively amongst Ascending Power Leaders.

At Ulta, amika’s Normcore Signature Shampoo and CÉCRED’s Clarifying Shampoo & Scalp Scrub (+44 ranks, momentum 3.4) are both ascending rapidly through targeted benefit ownership. Across both channels, the brands losing rank are the ones whose product naming has become generic – “hydrating shampoo,” “repair conditioner” – in a market that rewards the specific over the broad.

The Sephora Story: Prestige Holds, But Only Where It Has Earned the Right

At Sephora, the prestige tier is not losing, it is bifurcating.

Kérastase holds #1 overall with 8 products in the top 50 from 106 total, winning through formulation specificity (anti-breakage, oily scalp, heat damage, thickening) rather than heritage alone.

K18 holds #2 with just 14 products and a 36% top-50 penetration rate, the strongest concentration in the top 10, built entirely on a patented peptide biotechnology claim with no lifestyle overlay.

Dae (#3) and Gisou (#4), both Affordable, win through coherence: Gisou achieves a 100% top-50 penetration rate in S&C from just 4 SKUs.

The decliners, including Moroccanoil (90 products, 2 in the top 50), Living Proof (-21), and Nécessaire (-23), share one trait: benefit language too general to compel choice in a market that rewards the specific.

The standout momentum signal is Oribe’s Supershine Hydrating Conditioner at $20 climbing +140 ranks, the largest single delta in the Sephora S&C top 50. A Premium-Prestige brand at an affordable price point with a precise claim; the combination, not the tier, is what drove the result.

The Ulta Story: Professional Heritage Holds the Top, Science-Forward Challengers Climb Fast

At Ulta, Redken holds #1 with 10 products in the top 50 from 80 total, winning on professional salon credibility and protein-based formulation credentials at Masstige-Affordable Premium prices ($11-$36).

But the momentum data contains a warning the overall ranking obscures: its All Soft Shampoo, Acidic Bonding Concentrate line, and Frizz Dismiss range are all classified At-Risk Leaders with negative momentum scores, and the summary is blunt: “Legacy Bonding lines like Redken that only repair old damage are now being commoditized.”

The clearest signal of where Ulta is moving is CÉCRED at #6 (+7), whose Clarifying Shampoo & Scalp Scrub at $19 climbed 44 ranks with a momentum index of 3.4, projected to reach the top 5 within two quarters.

Alongside it, Nutrafol’s Root Purifier Scalp Microbiome Shampoo at $44 climbed +191 ranks (momentum 4.0), Bondi Boost’s thinning shampoo climbed +43, and isima, a brand entirely new to the top 50, placed two products with momentum scores of 2.0 and 4.4 respectively.

The Ascending Disruptor quadrant at Ulta is full of challengers that did not exist in the category’s top tier six months ago, and nearly all of them are built around scalp health, thinning, or microbiome science rather than bond repair.

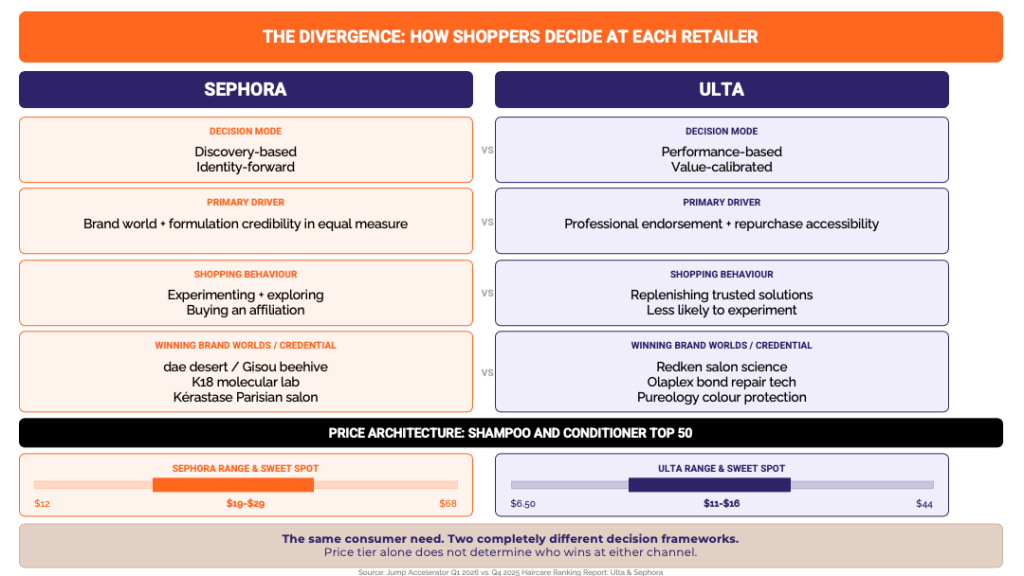

The Divergence: What Each Retailer's Rankings Reveal About Shopper Decision-Making

The most analytically useful finding from reading both datasets together is that the same underlying consumer desire for healthy, repaired, and beautiful hair is being resolved by fundamentally different decision frameworks depending on retail context.

At Sephora, the consumer is making a discovery-based, identity-forward choice. The brands that dominate combine a legible brand world (dae’s desert, Gisou’s beehive, K18’s molecular lab, Kérastase’s Parisian salon) with formulation credibility sufficient to justify the price. She is not simply buying a product; she is buying an affiliation. The premium she pays is partly for the formulation and partly for the identity the brand confers.

At Ulta, the consumer is making a performance-based, value-calibrated choice. The brands that hold the top positions have professional endorsement as their primary credential: salon brands that have migrated to the consumer channel with price points that remain accessible on a regular repurchase schedule. She is less likely to be experimenting and more likely to be replenishing.

The price architecture differs significantly between the two channels. Sephora’s Shampoo & Conditioner top 50 spans $12 (Pureology) to $68 (Kérastase Première Anti-Breakage Repairing Mask), with multiple brands finding momentum in the $19-$29 range. Ulta’s Shampoo & Conditioner top 50 is more compressed: $6.50 (Biolage Color Last), $9.50 (Paul Mitchell Tea Tree), $11 (Redken All Soft), $12 (Pureology), with the Affordable Premium ceiling represented by Redken’s $29-$36 range and only Nutrafol’s $44 scalp shampoo breaking meaningfully above that.

Biolage: The Ulta-Specific Story of Quiet Ascent

One of the most underreported brand stories in the Q1 data is Biolage’s rise to #4 at Ulta, up 4 places from Q4 2025, with 2 products in the top 50 and 4 in the top 100 from a 51-SKU portfolio.

Its Color Last Shampoo and Conditioner for color-treated hair at $6.50 is classified as Ascending Power Leaders, with the shampoo at #9 in the category.

Biolage’s positioning of botanical-inspired formulations delivering nature-derived salon-quality performance occupies a territory that is increasingly valuable at Ulta: professional-grade specificity (color protection, scalp care, hydration for very dry hair) at price points that make daily use economical. In a market where $11 Redken holds #1 and $6.50 Biolage holds #4, the Ulta consumer is demonstrating that professional endorsement combined with specific benefit and accessible price creates a value equation that requires no further justification.

Pureology: The Cross-Channel Constant

If amika is the clearest example of a brand winning both channels simultaneously, Pureology is the clearest example of a brand winning both through different mechanisms.

At Sephora, Pureology sits at #2 in shampoo and conditioner (up 1 from Q4), with 3 products in the top 20 and 4 in the top 50 from 23 total. That is a 75% top-20 penetration rate among its hero products, the highest in the Sephora S&C category. Its Hydrate Conditioner For Dry Hair at $12 climbed 30 ranks to #8 with a momentum score of 3.8, an Ascending Power Leader projected to reach #3 within two quarters.

At Ulta, Pureology holds #3 overall, with 3 products in the top 50 and 6 in the top 100 from 32 total. Its Hydrate Shampoo and Conditioner For Dry Hair anchor the top 10; its Strength Cure range is ascending steadily. The brand is classified Premium at Sephora and Affordable Premium at Ulta, a price tier differential reflecting the two channels’ respective customer baselines. The same products are winning in both contexts.

The Pureology case makes the argument that damage and hydration specificity, delivered at the $12 price point, is the most universally effective value equation in haircare retail right now. The consumer at Sephora and the consumer at Ulta both respond to “Hydrate Shampoo for Dry Hair at $12” because the benefit is legible, the price creates no hesitation, and the brand’s professional heritage removes the need to validate the claim.

The New Frontier: Scalp Science as the Next Category Battleground

The most significant directional signal in the combined Ulta-Sephora data is not happening in the established shampoo and conditioner mainstream. It is happening at the intersection of scalp health, thinning, and biotech, a territory that is ascending rapidly at Ulta and beginning to appear at Sephora, and that the current top-ranked brands are largely not occupying.

At Ulta: Nutrafol’s Root Purifier Scalp Microbiome Shampoo at $44 is climbing +191 ranks to #48 and is projected to reach the top 10 in two quarters. CÉCRED’s Clarifying Shampoo & Scalp Scrub at $19 climbed 44 ranks to #13 and is projected to reach the top 5. Bondi Boost’s HG Shampoo for Thinning Hair at $15 climbed 43 ranks to #16. These three products represent distinct price tiers and brand stories: Nutrafol (prestige-lux brand) is Clinical + Premium-Prestige SKU, CÉCRED SKU is affordable (brand, founded by Beyoncé, is salon-cultural, affordable-premium), Bondi Boost( affordable-premium brand) SKU is masstige.

But they share a common category thesis: the scalp, not the strand, is the next primary site of innovation and consumer spending in haircare.

At Sephora, Kérastase’s Densifique Thickening Shampoo for Thinning Hair climbed 30 ranks to #37 in S&C. Its Genesis Strengthening Scalp and Hair Serum holds the #1 position overall in the brand’s product ranking.

The scalp signal is present but less acute than at Ulta, likely because Sephora’s skincare-sophisticated consumer has been thinking about the scalp as “skin” for longer, making the category less disruptively new there and more of an established premium tier.

The unified read across both retailers is this: the scalp health category is in early-to-mid disruption at Ulta and moving from disruption to mainstream at Sephora.

Summary: What This Means for Founders, Retailers, Innovators And Investors

The Q1 2026 dual-retailer haircare data resolves into five findings that cut across both channels.

First, there is no single haircare consumer.

There are two, and they shop at different retailers.

The Sephora haircare shopper pays for brand world and formulation credibility in roughly equal measure and responds to discovery.

The Ulta haircare shopper pays for professional endorsement and specific functional performance at value-calibrated prices.

Brands cannot change their story for each retailer but they can emphasise different elements of story, choose different SKUs for trials, and customize shopper marketing by retailer.

Second, the bonding-chemistry wave is cresting, the scalp-biotech is building.

The At-Risk Leader classifications for Redken’s Acidic Bonding Concentrate line and the At-Risk Disruptor classification for Olaplex’s gift set at Ulta are early signals of commoditization in a category that drove significant premium growth over the past four years. Founders building in the damage-repair space need a story that goes beyond “bond repair.”

Molecular specificity (K18’s approach), scalp-origin differentiation (CÉCRED, Nutrafol), or ritual-world coherence (amika, dae) are the three architecture models the data supports as defensible.

Third, portfolio penetration is the defining metric of retail health, and it differs by channel.

At Sephora, the winning penetration model is concentrated depth: K18’s 36% top-50 penetration from 14 products, Gisou’s 100% top-50 penetration from 4 shampoo and conditioner SKUs.

At Ulta, the winning model allows for slightly broader deployment, as Redken’s 10 products in the top 50 from 80 total (12.5%) shows, but it still rewards focus over sprawl.

In neither channel does having 90, 106, or 140 products correlate with ranking dominance. What correlates is the percentage of the portfolio generating top-tier placement.

Fourth, new launches: mostly white space in the retailer's floor price tier

At Sephora’s $20-$30 Affordable tier, saw the highest no. of new launches, and the SKUs are genuinely filling gaps: Kenra Professional bringing accessible professional styling, Unove entering K-beauty repair science, and Bounce Curl addressing curl-specific formulations that prestige retail has largely ignored.

At Ulta’s $10-$20 Masstige tier saw the highest number of new launches. Kitsch, Kristin Ess, and Odele are correctly targeting the scalp health, curl care, and clean-natural territories that legacy professional brands have left open.

The white space reads as real for roughly two-thirds of the launches. The remaining third, predominantly dry shampoo and frizz control extensions from brands already present in those categories, is pile-on, not gap-filling, and those SKUs face the commoditization clock.

Fifth, and most broadly, the haircare category in 2026 is not bifurcating into "affordable wins" versus "prestige wins."

It is bifurcating into brands with a precise reason to exist at their price point and brands that are occupying space by inertia.

At Sephora, Kérastase at $22-$68 and dae at $16-$30 are both ascending because both have a precise reason to exist: one through formulation specificity, one through brand’s desert-inspired coherence.

At Ulta, CÉCRED at $19 and Nutrafol at $44 are both ascending for the same reason.

At both retailers, the brands losing rank share one thing in common: they no longer own a category claim specific enough to compel the consumer to choose them over a shelf of alternatives that are naming the problem more precisely.

The shelf, at Ulta and at Sephora, is running out of patience for the general.

Beauty reports & solutions for speed of sticky scale| 70+ brands grown