La Mer holds #1 at Nordstrom and Bloomingdale’s and #2 at Neiman Marcus. No Pure Indie brand appears in the top 50 at more than one retailer simultaneously. And yet Dr. Barbara Sturm, fully independent, holds #6 at Neiman. Biologique Recherche, family-owned since the 1970s, holds #6 at Bloomingdale’s. The luxury skincare department store landscape is more stratified, more data-driven, and more strategically navigable than the conventional narrative suggests. The top is locked. The path in exists. It does not look like what most founders expect.

Q1 2026 DATA: THREE RETAILERS

Nordstrom: 382 brands, 5,384 products

Neiman Marcus: 96 brands, 1,429 products

Bloomingdale’s: 143 brands, 2,242 products

9 price tiers mapped across all three.

The Context: A Channel Under Pressure

The luxury skincare department store channel entered 2026 under significant structural stress.

- Neiman Marcus filed for bankruptcy protection under Saks Global in January 2026, representing the most significant structural shift in US luxury retail in a decade

- Nordstrom and Bloomingdale’s were the only department stores to report higher average visits per venue in the second half of 2025 (Placer.ai data)

- Department stores are projected to lose share of beauty sales by 2030 while specialty retailers and online channels grow (McKinsey State of Beauty, 2025)

This context changes the strategic calculus for every audience reading this analysis. Nordstrom and Bloomingdale’s are not three equivalent retailers. One of the three is in active restructuring. The luxury skincare department store strategy for 2026 must account for that divergence.

The Honest Thesis

At the top 10, all three channels tell the same story.

- Nordstrom top 10: 90% Heritage brands, 60% Luxury tier, 60% Formulation and Function archetype

- Neiman Marcus top 10: 60% Heritage brands, 90% Luxury tier, 67% Formulation and Function archetype

- Bloomingdale’s top 10: 60% Heritage brands, 90% Luxury tier, split evenly across all three archetypes (formulation + functional, story + origin, ritual + sensorial)

Heritage brands dominate the top 10 everywhere. Indie brands do not break through the top 10 at Nordstrom or Neiman. Bloomingdale’s is the single exception.

The divergence that matters for luxury skincare department store strategy lives in ranks 11 to 50.

- Nordstrom opens to 8 price tiers from rank 11 including Masstige and Affordable

- Neiman stays Luxury-dominant through rank 30 before other tiers appear

- Bloomingdale’s holds Luxury concentration through rank 40, the tightest mid-ranking of the three

The one-line summary: Nordstrom she discovers. Neiman she replenishes. Bloomingdale’s she selects.

The distinction matters. At Neiman, the shopper curates her own basket from a Heritage universe she already knows. At Bloomingdale’s, the retailer has curated the assortment and the shopper trusts that edit, including channel-exclusive brands she cannot find anywhere else.

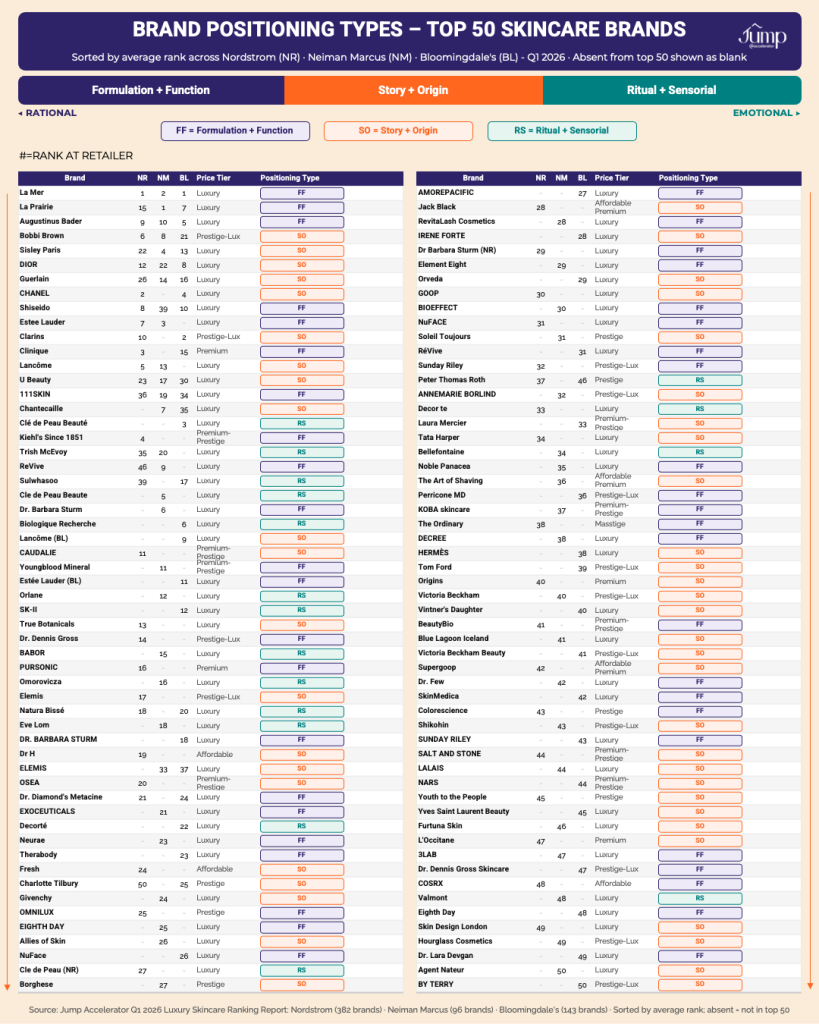

The Three Positioning Types

Every brand at department store skincare wins through one of three positioning mechanisms. These map directly to the positioning spectrum from Rational to Emotional.

Formulation and Function (left of spectrum: Ingredients/Process and Functional Benefits) Wins because the shopper believes the product delivers a specific, clinical, measurable result.

- La Mer, Augustinus Bader, Dr. Barbara Sturm, Clinique, La Prairie, Shiseido, Estée Lauder

- 60% of the top 10 at Nordstrom, 67% at Neiman, 40% at Bloomingdale’s

- 40% of the top 50 across all three channels

Story and Origin (middle of spectrum: Purity/Source through Emotional Promise and Purpose) Wins because of where the brand comes from, what it stands for, who founded it, or the identity it confers.

- CHANEL, DIOR, Guerlain, Lancôme, Sisley Paris, Clarins, CAUDALIE, Tata Harper, True Botanicals

- The largest archetype in the top 50 across all three channels: 48% at Nordstrom, 45% at Neiman, 46% at Bloomingdale’s

- Dominates the mid-ranking (11 to 50) at every retailer

Ritual and Sensorial (right of spectrum: Experiential dominant) Wins because using the product is itself the luxury. Texture, scent, ceremony, and pleasure drive purchase and repeat.

- Biologique Recherche, Valmont, Clé de Peau Beauté, Sulwhasoo, Natura Bissé, Omorovicza, BABOR

- The smallest archetype: 12-15% of the top 50 across all three channels

- Commands the highest prices and deepest loyalty when it works

- Zero top 10 positions at Nordstrom and Neiman, 20% at Bloomingdale’s

The La Mer exception: La Mer is the only brand competing credibly across all three archetypes simultaneously.

- Formulation: Miracle Broth fermented marine complex, deep hydration and renewal

- Story: Iconic luxury heritage, origin narrative built over decades

- Ritual: Indulgent texture experience as a core product promise

- This multi-archetype position explains why it holds #1 at two of three retailers and #2 at the third. No other brand in this analysis achieves it.

RETAILER PROFILE

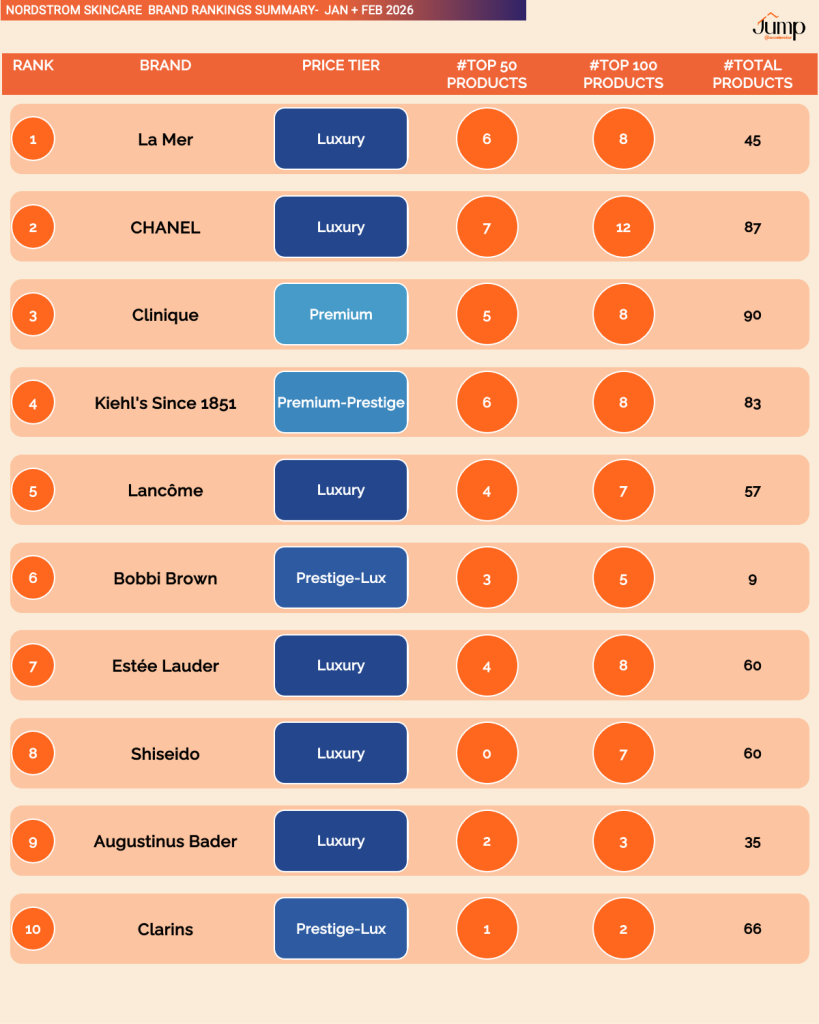

Retailer Profile 1: Nordstrom

The shopper: Early Mainstream. Exploring prestige and luxury skincare, not yet fully committed to it. Open to Premium-Prestige and Prestige pricing alongside Luxury.

What makes Nordstrom different:

- Only channel where Premium (Clinique #3) and Premium-Prestige (Kiehl’s #4) outrank Luxury brands in the top 5

- 8 price tiers in the top 50, from Masstige ($11) to Luxury ($500+)

- Formulation and Function brands dominate the top 10 (60%)

- Story and Origin brands dominate the full top 50 (48%)

- The Ordinary at #38, COSRX at #48, Jack Black at #28: none appear at Neiman or Bloomingdale’s top 50

- The mid-ranking (11 to 50) includes brands that would not pass the entry filter at the other two channels

The honest challenge: The top 10 at Nordstrom is 90% Heritage. Discovery happens in ranks 11 to 50, not at the top.

The Clinique and Kiehl’s signal: These two brands outranking Estée Lauder, Shiseido, and Augustinus Bader is not a stocking decision. It reflects actual purchase behavior. The Nordstrom skincare shopper chooses accessible prestige over full Luxury at a rate the other two channels’ shoppers do not.

Price architecture:

- Full range: $11 (Masstige) to $500+ (Luxury)

- Sweet spot for competitive entry: Premium-Prestige to Prestige-Lux ($41-$80)

- 8 tiers represented: the most price-diverse channel of the three

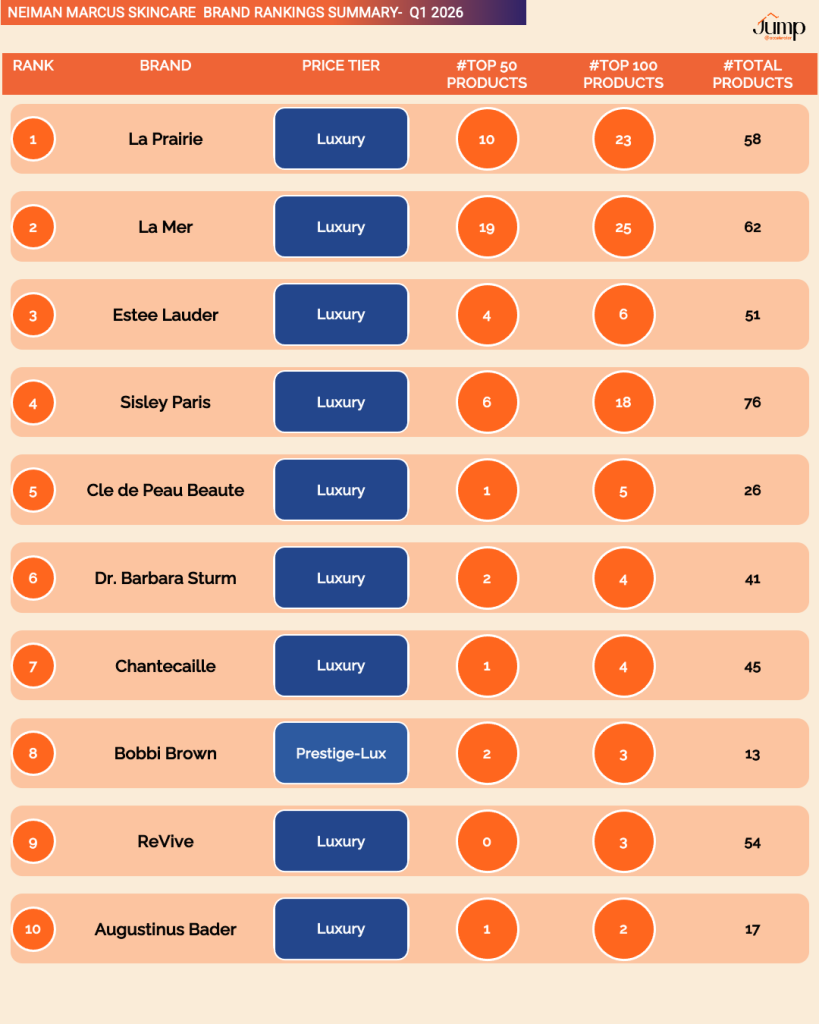

Retailer Profile 2: Neiman Marcus

Critical context: Neiman Marcus filed for bankruptcy protection under Saks Global in January 2026. Its Q1 2026 rankings reflect the pre-restructuring brand hierarchy. Any luxury skincare department store strategy targeting Neiman must account for an assortment, distribution, and service model that is actively in transition.

The shopper: Late Mainstream. High brand loyalty, high repeat rate, low tolerance for anything below unambiguous Luxury status. Not experimenting. Replenishing.

What makes Neiman different:

- 90% Luxury in the top 10 and 90% Luxury through rank 30: the most tier-locked channel

- Formulation and Function brands dominate the top 10 (67%), the highest of the three retailers

- La Prairie at #1 with 10 top-50 products from 58 total: the strongest single-brand loyalty signal in this analysis

- Dr. Barbara Sturm at #6, Pure Indie, fully independent: clinical science at Luxury pricing gains traction even at the most Heritage-loyal channel

- ReVive at #9 with 54 total products but zero in the top 50: rank held entirely on existing consumer loyalty, zero new product traction

The loyalty channel evidence: ReVive at #9 with zero top-50 products from 54 SKUs therefore means: discovery is weak (no product breaking through on new trial volume), but loyalty is sufficient to hold the overall brand rank. The brand is surviving on its existing consumer base replenishing, not growing.

Price architecture:

- Full range: $31 (Affordable Premium) to $500+ (Luxury)

- Sweet spot: Luxury and Prestige-Lux ($61-$500+)

- 5 tiers represented: the most Luxury-concentrated channel

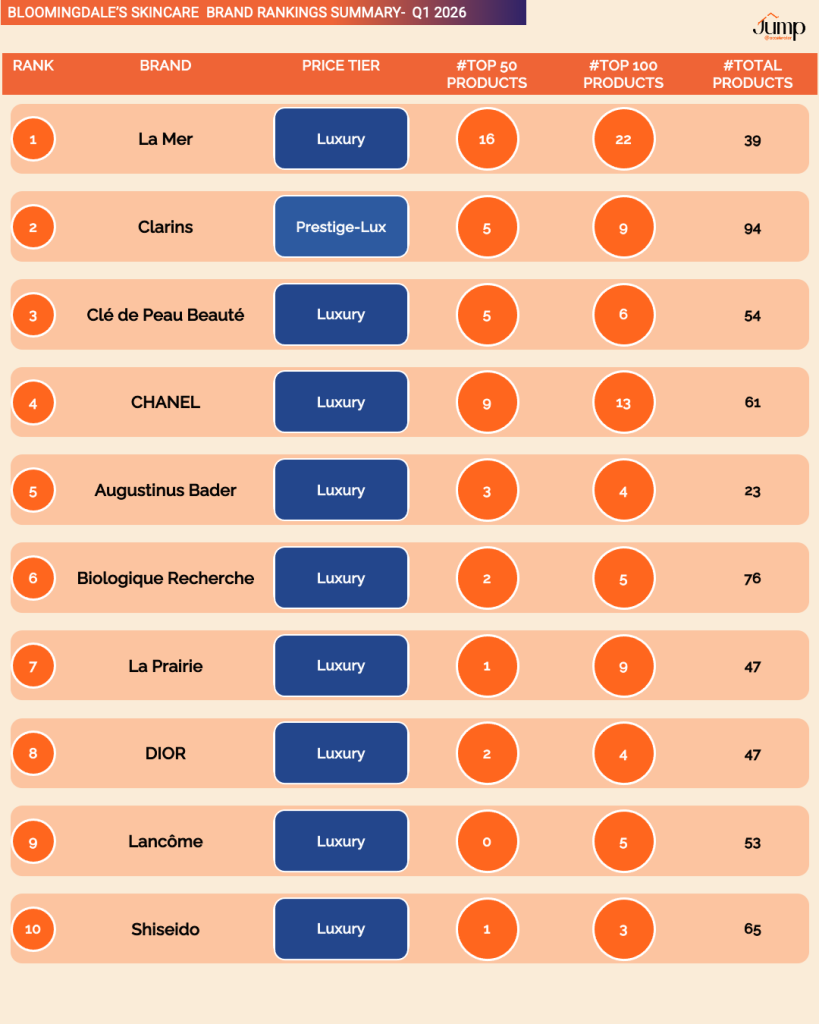

Retailer Profile 3: Bloomingdale’s

Critical context: Bloomingdale’s is gaining market share as Neiman Marcus restructures. It reported a 0.8% increase in average visits per venue in the second half of 2025, actively adding niche and emerging luxury skincare brands, and is the channel best positioned to absorb the Neiman Marcus shopper at the luxury tier.

The shopper: Mid-Mainstream. She trusts the retailer’s edit. Bloomingdale’s has made channel-specific assortment decisions including brands not available at Nordstrom or Neiman and she shops within that curated universe. She buys deep into what she selects rather than sampling widely.

What makes Bloomingdale’s different:

- La Mer: 16 products in the top 50 from just 39 SKUs, 41% penetration, the highest of any brand across all three retailers

- Clarins at #2: Prestige-Lux, the only non-Luxury brand in the top 5 at either Neiman or Bloomingdale’s

- Biologique Recherche at #6: channel-exclusive, Ritual and Sensorial archetype, not in Nordstrom or Neiman top 50

- The most balanced top 10 across all three archetypes: 40% Formulation, 40% Story, 20% Ritual

- Luxury concentration holds through rank 40, the tightest mid-ranking of the three

The curation channel evidence:

- La Mer: 41% top-50 penetration from 39 SKUs

- Augustinus Bader: 13% from 23 SKUs

- Clé de Peau Beauté: 9.3% from 54 SKUs

Shoppers are buying deep into specific brands, not sampling across many. That is the curation signal.

The Biologique Recherche signal: Holds #6 at Bloomingdale’s with 2 top-50 products from 76 SKUs. Wins entirely through a protocol-based, skin-analysis-led service model. The ranking depends on the beauty counter functioning as a service delivery point. Remove the service infrastructure and the ranking collapses.

Price architecture:

- Full range: $36 (Premium) to $500+ (Luxury)

- Sweet spot: Luxury and Prestige-Lux ($61-$500+)

- 5 tiers represented, Luxury dominant through rank 40

The Cross-Channel Signals

La Mer: the only true cross-channel dominant.

- #1 Nordstrom, #2 Neiman, #1 Bloomingdale’s

- The only brand competing across all three positioning archetypes

- Hero SKU concentration drives performance at every channel, not portfolio breadth

- Portfolios of 39 to 62 SKUs per channel, always with the Moisturizing Cream as anchor

La Prairie: wins Neiman, fragile at Bloomingdale’s.

- #1 Neiman with 10 top-50 products from 58 total (17% penetration)

- #7 Bloomingdale’s with 1 top-50 product from 47 total (2.1% penetration)

- Same Luxury tier, similar portfolio, entirely different shopper relationship

- The Neiman Marcus bankruptcy makes La Prairie’s channel concentration risk more acute

Augustinus Bader: the cross-channel compounder.

- Top 10 at all three retailers from portfolios of 17 to 35 SKUs

- Pure Formulation and Function archetype with no heritage or ritual overlay

- The only Minority-Backed Independent with cross-channel top 50 presence

- Winning entirely on formulation belief and word-of-mouth advocacy built outside the store

No Pure Indie brand holds top 50 at more than one retailer simultaneously.

- The two channel-specific exceptions (Dr. Barbara Sturm at Neiman #6, Biologique Recherche at Bloomingdale’s #6) were built through mechanisms that require years to replicate at a second channel

- This is the single most important data point for founders and investors considering luxury skincare department store strategy

The indie brand percentage by retailer tells a more nuanced story.

Neiman Marcus has the highest indie brand presence: 58% of its top 50 are Indie or Emerging – but this is pre-bankruptcy data and every brand is priced at Luxury tier ($80+) Bloomingdale’s follows at 52% and is the more actionable signal: gaining market share, actively adding emerging Luxury brands, Pure Indie brands already in the top 10

Nordstrom has the lowest indie presence at 32% but accepts the widest price range – correct entry point for brands not yet at Luxury pricing

The first door depends on your price tier, not on overall indie percentages

The Opportunity: Department Stores as Discovery, Loyalty, and Advocacy Bastions for Luxury

This is the strategic reframe the luxury skincare department store channel needs most urgently.

The problem with the current model:

- Department stores are not losing to Sephora at Masstige or Affordable tier. They were never competing there.

- Their structural advantage is Luxury and above, where no other retail format can replicate the service model, the environment, or the shopper relationship

- The current model treats the beauty counter as a display and transaction function

- The opportunity is to treat it as a Discovery, Loyalty, and Advocacy engine specifically for the Luxury tier

Why Luxury tier new brand launches are rare:

- Launching at Luxury pricing requires formulation investment, brand credibility, and service infrastructure most founders cannot access at launch

- Heritage Corporate and Heritage Independent brands that dominate were almost all built over 20-plus years

- This makes the Luxury tier the least crowded from a new entrant perspective at the moment new shopper demand for it is growing fastest

- That gap is the department store’s opportunity: curating and incubating the next generation of Luxury brands before any other channel discovers them

The store-within-a-store model:

- Blue Mercury inside Macy’s is the right analogy: a curated luxury beauty concept with its own service model and shopper loyalty operating inside the host retailer

- Bloomingdale’s is closest to this already: Biologique Recherche at #6 is effectively a clinic within the beauty floor

- Nordstrom can build the same for emerging Formulation and Function brands at Premium-Prestige to Prestige tier

- The Neiman Marcus restructuring creates an opening: the Saks Global model, if executed well, can rebuild the Neiman beauty counter as a curated Luxury skincare destination rather than a Heritage-only holdout

The three roles the channel can own:

Discovery: identify and incubate new Luxury and Prestige-Lux brands before any other channel carries them.

- Story and Origin archetype brands dominating the mid-ranking need a physical, curated space to tell their story

- First-mover curation of the next Luxury brand generation is the highest-return category investment available

Loyalty: the beauty advisor relationship drives retention at rates no digital or specialty channel matches.

- Systematically invest in advisor education, sampling, and referral programs

- Deepen the loyalty cycle with existing shoppers before the cohort ages out

Advocacy: treat the beauty advisor as a seeded referral network, not a display executor. Go beyond, curate indie brands with a strong advocacy engine and design an advocacy strategy for your beauty store to become the most talked about destination for luxury indie brands.

- A shopper who converts at a Luxury counter generates two to three referred shoppers through word-of-mouth

- That advocacy chain is the growth engine the channel is currently leaving unused

The Strategic Roadmap for Indie Brands at Luxury Department Store

What does not work:

- Launching with a broad range of 20-plus SKUs across categories

- Relying on the retailer’s foot traffic for shopper acquisition

- Running promotional events and gift-with-purchase to drive trial

- Entering below Luxury pricing at Neiman or Bloomingdale’s without decades of loyalty equity

The roadmap that works: Advocacy-Led Retail Entry

Step 1: Build advocacy pull before the store.

- The shopper must arrive pre-sold: dermatologist referral, editorial credibility, word-of-mouth, or protocol reputation built outside the department store

- Dr. Barbara Sturm at Neiman #6 and Biologique Recherche at Bloomingdale’s #6 both demonstrate this

- The store is the conversion point, not the discovery point

Step 2: Choose your first door by price tier.

If priced below $61 (Premium-Prestige or Prestige): enter Nordstrom first.

– The only channel where sub-Luxury tiers hold ranked positions in the top 50

– Build velocity proof and top-20 rank evidence within your tier before approaching higher-tier channels

If priced at Luxury ($80+) with advocacy pull already built: enter Bloomingdale’s first.

– Highest actionable indie brand presence of the three active channels at 52% of top 50

– Gaining market share post-Neiman bankruptcy, actively adding emerging Luxury brands

– Its top 10 already includes Pure Indie brands, making it structurally more open to new Luxury entrants than Nordstrom

– Then approach Neiman post-restructuring once Bloomingdale’s rank is established

Step 3: Enter with under 12 SKUs and one dominant hero.

- La Mer wins at 41% penetration from 39 SKUs. Augustinus Bader wins cross-channel from 17 to 35 SKUs per channel.

- One hero product that turns fast and generates repeat purchase outperforms 20 SKUs with low individual turns

- The retailer’s metric is profit per square foot, not SKU count

Step 4: Choose your positioning archetype and commit.

- Formulation and Function: dominant top-10 archetype at Nordstrom and Neiman. Requires a specific, defensible clinical credential.

- Story and Origin: dominant top-50 archetype at all three channels. Requires a genuine, specific origin the beauty advisor can tell in 30 seconds.

- Ritual and Sensorial: smallest archetype but deepest loyalty driver. Only works where the beauty counter functions as a service point.

Step 5: Price at Luxury for Neiman or Bloomingdale’s.

- Only one non-Luxury brand holds a top-10 position at either channel: Clarins at Bloomingdale’s #2, built on 30-plus years of loyalty and 94 SKUs

- A new brand entering below Luxury without that loyalty history competes with a structural disadvantage no marketing spend corrects

- If the formulation and story cannot justify Luxury pricing, Nordstrom at Premium-Prestige is the correct first door

What This Means

For Founders

- Department store luxury skincare is not a first door. Enter specialty before any department store channel.

– Below $61: enter Nordstrom first. The only department store accepting sub-Luxury pricing in meaningful numbers.

– At Luxury ($80+) with advocacy already built: enter Bloomingdale’s first. It has 52% indie presence, growing foot traffic, and is best positioned to absorb the post-Neiman luxury shopper. - Choose one positioning archetype and build everything around it. The beauty advisor has 30 seconds to make the recommendation.

- Build advocacy pull before you approach the retailer. The shopper must arrive asking for you by name.

- Launch under 12 SKUs with one hero product. Profit per square foot is the retailer’s metric, not SKU count.

- Price at Luxury for Neiman and Bloomingdale’s. Anything less is a structural disadvantage.

- The Neiman Marcus restructuring is an opportunity, not a deterrent. A rebuilt Neiman beauty counter under Saks Global may be more open to emerging Luxury brands than the pre-restructuring model was.

For Investors

- Watch penetration rate trajectory from small portfolios, not overall rank position.

- Augustinus Bader: top 10 at all three retailers from under 35 SKUs, improving penetration across all three, the only Minority-Backed Independent with cross-channel presence. This is what compounding retail equity looks like before it shows in revenue.

- Brands with 50-plus SKUs and under 5% top-50 penetration have stalled on discovery while loyalty holds the rank. Shiseido at 0% top-50 penetration, ReVive at 0%, Clarins at 5.3%. When the loyal cohort ages out there is no discovery pipeline to replace it. That is the declining asset.

- Formulation and Function archetype brands with cross-channel presence and small portfolios represent the highest-conviction bets. Story and Origin archetype brands dominating the mid-ranking represent the discovery pipeline.

- The Neiman Marcus bankruptcy creates a redistribution of luxury skincare shopper loyalty. Brands with cross-channel presence at Nordstrom and Bloomingdale’s are best positioned to capture it.

- Pure Indie brands with cross-channel ambition require a 3 to 5 year advocacy-led retail build. Fund the roadmap, not just the door opening.

For Retailers

- Reframe the beauty counter from a display function to a Discovery, Loyalty, and Advocacy engine for Luxury and above.

- The correct diagnostic for shelf rationalization is top-50 penetration rate relative to total SKU count, not overall brand rank.

- Actively curate Story and Origin archetype brands at Luxury tier. New Luxury brand launches are rare. First-mover curation of the next generation is the highest-return investment available.

- The store-within-a-store model (Blue Mercury inside Macy’s) is the template. Dedicated service, own curation logic, own shopper loyalty.

- Beauty advisor advocacy programs treated as seeded referral networks are the highest-ROI growth lever at zero incremental acquisition cost.

- Bloomingdale’s has the clearest opportunity to absorb the Neiman Marcus luxury skincare shopper. The assortment, service model, and curation investment required to do so is the most time-sensitive strategic decision in US luxury beauty retail right now.

For Innovators

- Innovation Stopover 1 (same problem, same solution, higher quality) is fully occupied at Luxury tier. Competing with La Mer, La Prairie, and CHANEL on moisturizing and anti-aging territory they have owned for decades is the hardest entry point in luxury skincare.

- Stopover 2 (same problem, unique solution) is where successful indie brands broke through: Augustinus Bader’s TFC8, Biologique Recherche’s protocol model, Dr. Barbara Sturm’s molecular cosmetics. Unique solution at Luxury pricing, focused portfolio, pre-built advocacy.

- Stopover 3 (unique problem, unique solution) is almost entirely unoccupied in department store skincare: microbiome disruption, circadian rhythm formulation, epigenetic aging absent from the top 20 at all three retailers. The clearest white space in luxury skincare department store strategy for 2026.

- Ritual and Sensorial is underrepresented everywhere (12-15% of top 50) but commands the highest prices and deepest loyalty. A genuinely new ritual concept backed by credible formulation science has clear white space across all three channels.

SUMMARY

The luxury skincare department store channel is not dying. The brands and retailers treating it as though nothing has changed are the ones making it look that way.

- The top 10 is Heritage-locked at all three retailers, but 32-58% of the top 50 are indie and emerging brands, which means the mid-ranking is more open than it looks

- La Mer holds #1 at Nordstrom and Bloomingdale’s simultaneously from a focused 39-62 SKU portfolio – concentration beats breadth at every channel

- No Pure Indie brand holds top 50 positions at more than one retailer – the path in exists but it is advocacy-led, not acquisition-led

- Neiman Marcus filed for bankruptcy in January 2026 – Bloomingdale’s is the channel best positioned to absorb its luxury skincare shopper

- The brands and retailers that win from here treat the beauty counter as a Discovery, Loyalty, and Advocacy engine for Luxury, not a display shelf

Source:

Jump Accelerator Q1 2026 Skincare Ranking Report: Nordstrom (382 brands, 5,384 products, Jan-Feb 2026), Neiman Marcus (96 brands, 1,429 products), Bloomingdale’s (143 brands, 2,242 products).

Market references: Circana US Beauty H1 2025, McKinsey State of Beauty 2025, Placer.ai department store traffic data 2025, Business of Fashion March 2026, BeautyMatter March 2026.

Want to scale your beauty brand? Or Develop your beauty category?

JUMP ACCELERATOR:

Speed of sticky scale fueled by decoded market intelligence| 70+ brands scaled